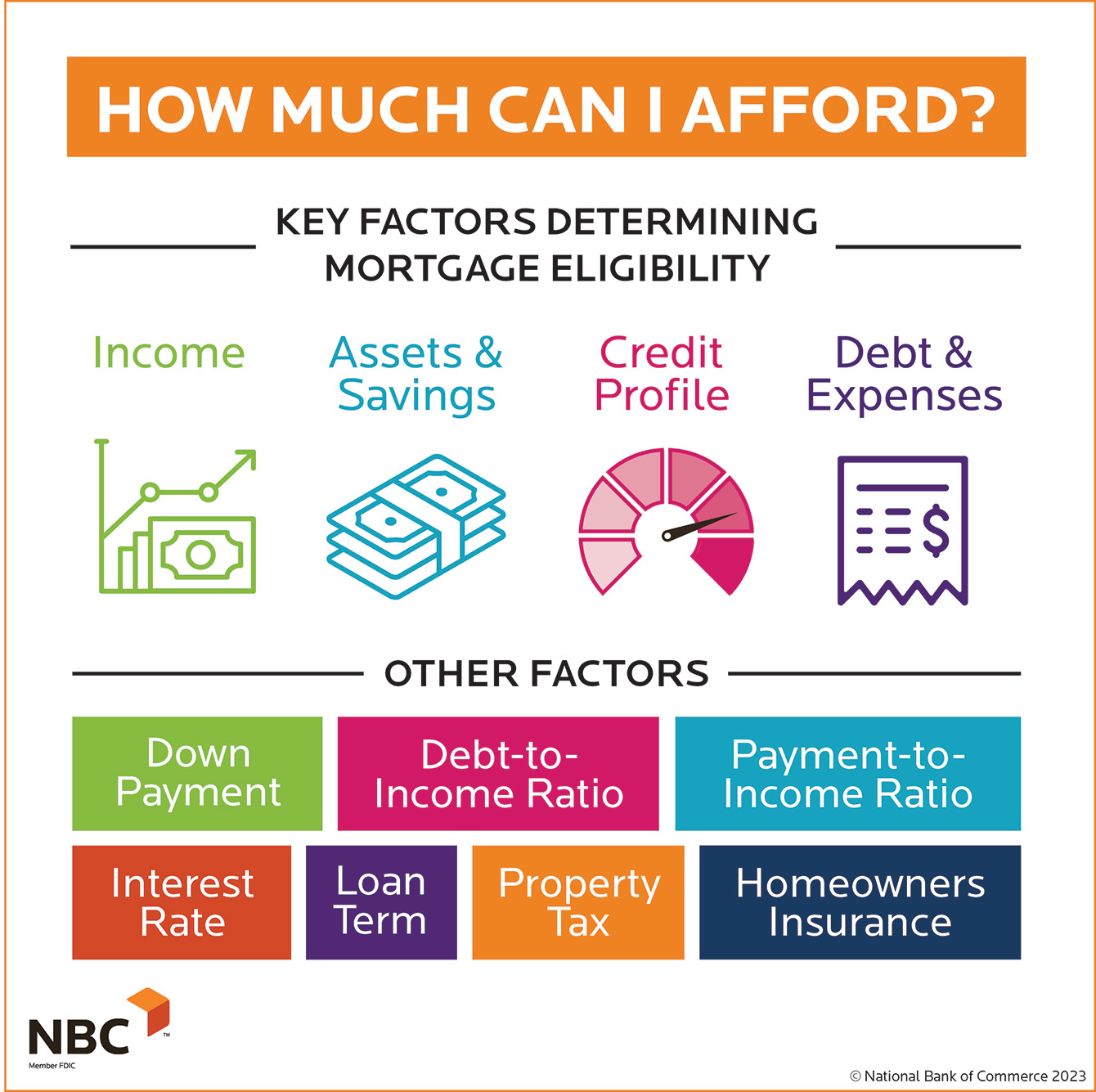

Qualifying for a loan can be a daunting task, especially for those who are new to the borrowing process. Lenders typically evaluate an individual’s creditworthiness based on several key factors, including credit score, income, debt-to-income ratio, and employment history. Understanding these requirements is crucial to determining the likelihood of loan approval. By grasping the essential criteria that lenders use to assess loan applications, individuals can take proactive steps to improve their chances of qualifying for a loan. A well-prepared loan application can make all the difference in securing the necessary funds.

Understanding the Loan Qualification Process

To qualify for a loan, you need to meet certain criteria set by lenders. The qualification process typically involves an evaluation of your creditworthiness, income, and other financial factors. Lenders use this information to determine the likelihood that you will repay the loan. Credit score plays a significant role in this process, as it reflects your history of managing debt. Other factors such as debt-to-income ratio, employment history, and collateral (for secured loans) are also considered.

Evaluating Your Creditworthiness

Your creditworthiness is a crucial factor in determining whether you qualify for a loan. Lenders typically review your credit report to assess your credit history, including past payments, outstanding debts, and any negative marks such as bankruptcies or foreclosures. A good credit score can significantly improve your chances of qualifying for a loan with favorable terms. To enhance your creditworthiness, focus on making timely payments, reducing debt, and monitoring your credit report for errors.

Loan Repayment Strategies

Loan Repayment StrategiesAssessing Your Income and Debt-to-Income Ratio

Lenders also evaluate your income and debt-to-income (DTI) ratio to ensure you can afford the loan payments. Your DTI ratio is calculated by dividing your total monthly debt payments by your gross income. A lower DTI ratio indicates a more manageable debt burden. To qualify for a loan, you should aim for a DTI ratio of 36% or less. You can improve your DTI ratio by increasing your income, reducing debt, or avoiding new debt obligations.

Preparing Required Documentation

To qualify for a loan, you will need to provide various documents to support your application. These may include proof of income, identification, and bank statements. Having these documents ready can streamline the application process and help lenders assess your creditworthiness more efficiently. Ensure that your documents are up-to-date and accurately reflect your financial situation.

| Required Documents | Purpose |

|---|---|

| Proof of Income | Verifies your income and employment status |

| Identification | Confirms your identity and age |

| Bank Statements | Provides insight into your financial transactions and account balances |

Frequently Asked Questions

What are the basic requirements to qualify for a loan?

To qualify for a loan, you typically need to meet certain basic requirements, including being at least 18 years old, having a stable income, and a good credit history. Lenders also consider your debt-to-income ratio and employment history. You will need to provide identification, proof of income, and other financial documents to support your loan application.

Impact of Loans on Credit Score

Impact of Loans on Credit ScoreHow does credit score affect loan qualification?

Your credit score plays a significant role in determining your eligibility for a loan. A good credit score indicates to lenders that you are a responsible borrower and can repay the loan on time. A higher credit score can help you qualify for better loan terms, including lower interest rates and larger loan amounts. Generally, a credit score of 700 or higher is considered good.

What is the debt-to-income ratio, and how does it impact loan qualification?

The debt-to-income ratio is the percentage of your monthly gross income that goes towards paying debts. Lenders use this ratio to assess your ability to manage your debt payments. A lower debt-to-income ratio indicates that you have a more manageable debt burden and are more likely to qualify for a loan. Typically, lenders prefer a debt-to-income ratio of 36% or less.

Can I qualify for a loan with a bad credit history?

While having a bad credit history can make it more challenging to qualify for a loan, it’s not impossible. Some lenders specialize in offering loans to individuals with poor credit. However, you may face higher interest rates or stricter loan terms. You can also consider alternatives, such as a secured loan or a co-signer, to improve your chances of qualifying for a loan.

Refinancing Loan Options

Refinancing Loan Options